English

English  Español

Español  Русский

Русский  Turkish

Turkish  Persian (فارسی)

Persian (فارسی)  Arabic (العربية)

Arabic (العربية)  简体中文 (中国)

简体中文 (中国)

ITAR Brokering in Foreign Defense Transactions: DS-4294 Approval, Expanding Enforcement, and Hidden Liability Risks

Brokering under the International Traffic in Arms Regulations (ITAR) is one of the most misunderstood and increasingly enforced areas of U.S. export control law. Many market participants assume the rules mainly apply to manufacturers and exporters. In reality, enforcement often focuses on intermediaries: consultants, introducers, deal facilitators, and even financial actors involved in defense-related transactions.

Under 22 C.F.R. Part 129, brokering activities tied to defense articles or defense services may require prior approval from the Directorate of Defense Trade Controls (DDTC). This applies even if the broker is not a U.S. manufacturer or exporter and in some cases, even if they are not physically located in the United States.

The risk is amplified by several factors:

- Broad, function-based definitions of what qualifies as “brokering activity”

- An increasingly assertive extraterritorial enforcement approach

- Close scrutiny of compensation structures, including success fees and commissions

- Overlapping exposure under sanctions, anti-corruption laws, and financial regulations

In practice, ITAR brokering risk often sits exactly where many firms assume it doesn’t: at the intersection of deal-making and facilitation.

What Constitutes “Brokering” Under ITAR

ITAR defines brokering in expansive and functional terms. Covered activities include:

- Arranging or facilitating the manufacture, export, reexport, or transfer of defense articles

- Negotiating contracts involving defense articles or defense services

- Acting as an intermediary between buyers and sellers

Notably, physical possession or handling of defense articles is not required to trigger regulatory exposure.

Common Misconception

“We only introduce parties. We do not participate in the transaction.”

This assumption is legally incorrect. Such introductions frequently fall squarely within the regulatory definition of brokering.

High-Risk Activities

- Introducing foreign government buyers to U.S. defense contractors

- Structuring or advising on defense procurement transactions

- Providing technical input regarding defense articles

- Facilitating financing tied to defense-related transactions

DS-4294 Approval: Transaction-Specific Authorization

Certain brokering activities require prior authorization through Form DS-4294, which must be obtained before engaging in any covered activity.

Key Characteristics

- Authorization is transaction-specific, not a general license

- Requires detailed disclosure of:

- All parties, including beneficial owners

- Defense articles and/or services involved

- End-use and end-user

- Transaction structure and valuation

Practical Reality

Directorate of Defense Trade Controls (DDTC) evaluates not only the technical compliance of the transaction, but also:

- Geopolitical and national security considerations

- End-user and jurisdictional risk profiles

- Credibility and compliance posture of intermediaries

- Potential sanctions or diversion risks

Extraterritorial Reach: Non-U.S. Brokers Are Not Safe

ITAR brokering provisions apply broadly to:

- U.S. persons acting globally

- Foreign persons located within the United States

- Foreign persons operating abroad in connection with U.S.-origin defense articles

Enforcement Trend

The Directorate of Defense Trade Controls has increasingly asserted jurisdiction in circumstances where:

- U.S.-origin defense articles are implicated

- U.S. financial systems or dollar-clearing mechanisms are utilized

- U.S. persons are involved, even indirectly

Implications

Non-U.S. intermediaries operating outside the United States may nonetheless face:

- U.S. enforcement exposure

- Transactional disruption or blocking

- Secondary consequences, including banking restrictions, sanctions exposure, and reputational harm

Enforcement Landscape: From Compliance Failure to Strategic Risk

ITAR brokering violations frequently arise from structural misunderstandings rather than intentional misconduct.

Common Violations

- Failure to register as a broker

- Engaging in brokering without required DS-4294 approval

- Incomplete or inaccurate disclosures

- Unauthorized expansion beyond approved activities

- Improper or non-compliant compensation structures

Enforcement Consequences

- Significant civil monetary penalties

- Consent agreements imposing multi-year compliance obligations

- Debarment from participation in defense trade

- Severe reputational and commercial consequences

In aggravated cases, violations may escalate to criminal liability, particularly where willfulness, false statements, or sanctions evasion is implicated.

Compensation Structures: The Hidden Liability Vector

Compensation structuring represents one of the most underappreciated sources of liability in ITAR brokering.

High-Risk Structures

- Success fees tied to transaction value

- Commission-based compensation linked to defense sales

- Payment routing through third countries or intermediaries

These arrangements may independently trigger exposure under:

- ITAR brokering provisions

- Anti-corruption regimes, including the Foreign Corrupt Practices Act (FCPA)

- Sanctions compliance frameworks

Practical Risk

Even where the underlying transaction is lawful, the compensation mechanism itself may create independent regulatory liability.

Intersection with OFAC, BIS, and Sanctions Regimes

ITAR compliance must be evaluated within a broader regulatory ecosystem.

A single transaction may simultaneously implicate:

- ITAR (defense articles and services)

- EAR (dual-use items regulated by BIS)

- OFAC-administered sanctions programs

Critical Insight

This multi-layered exposure is particularly acute in:

- Middle East transactions

- CIS jurisdictions

- African defense procurement markets

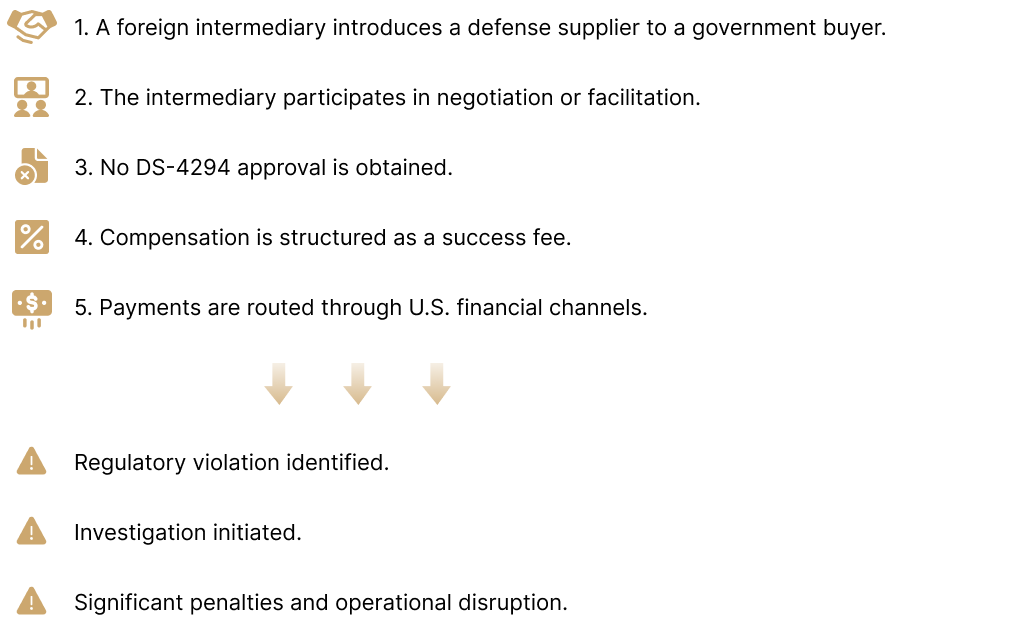

VIII. Case Pattern: Where Deals Fail

A recurring enforcement scenario typically involves:

Compliance Framework: Risk Mitigation Strategies

A defensible ITAR brokering compliance framework should include:

1. Activity Mapping

Identify whether any role or function constitutes “brokering” under ITAR definitions.

2. Registration Analysis

Assess whether broker registration requirements are triggered.

3. Pre-Transaction Review

Determine whether DS-4294 approval is required prior to engagement.

4. Counterparty Due Diligence

- Beneficial ownership analysis

- Sanctions screening

- End-use and end-user verification

5. Compensation Structuring

Ensure that compensation mechanisms do not create standalone liability.

6. Cross-Regime Integration

Coordinate ITAR compliance with OFAC and BIS regulatory requirements.

Frequently Asked Questions (FAQ)

What qualifies as brokering under ITAR?

Any activity facilitating a defense transaction on behalf of another—including introductions, negotiations, financing, or structuring—may qualify.

Do introductions alone trigger ITAR?

Yes. Even passive introductions may constitute brokering depending on the factual context.

Is DS-4294 always required?

No. However, it is required in many controlled scenarios under Part 129 and must be assessed prior to engagement.

Can foreign brokers be liable?

Yes. ITAR has demonstrable extraterritorial reach.

Are there exemptions?

Yes, but they are narrow, fact-specific, and frequently misapplied.

Does brokering apply to foreign-origin defense items?

Yes. ITAR brokering rules are not limited to U.S.-manufactured items.

Are there reporting obligations?

Yes. Annual reporting obligations may apply even after approval.

Why are success fees risky?

Because they may independently trigger liability under ITAR, FCPA, and Part 130 reporting requirements.

Real Enforcement Examples

Example 1 – Unauthorized Brokering (Island Pyrochemical Case)

DDTC alleged unauthorized brokering involving foreign-origin defense articles transferred from China to Brazil. The intermediary coordinated negotiations, pricing, and shipment without required approval.

Penalty: Approximately $850,000 (partially suspended subject to compliance remediation).

Key Takeaway:

Brokering exposure applies to foreign-origin items and indirect facilitation.

Example 2 – False Statements in Licensing

In the same matter, DDTC alleged misrepresentation of manufacturers and transaction details in licensing submissions.

Key Takeaway:

Documentation deficiencies may independently trigger enforcement, even where a transaction may otherwise have been licensable.

Example 3 – Compliance Program Failures

DDTC guidance emphasizes that failure to implement internal brokering controls—including approval procedures, reporting systems, and recordkeeping—constitutes a standalone enforcement risk.

Key Takeaway:

Brokering must be treated as an independent compliance function.

Example 4 – Proscribed Country Exposure

Transactions involving ITAR §126.1 countries significantly increase enforcement exposure and often preclude reliance on exemptions.

Practical Business Scenarios

Scenario A — The Introducer

A consultant introduces a defense supplier to a foreign government and participates in pricing discussions.

→ Likely constitutes brokering activity.

Scenario B — The Success-Fee Advisor

An intermediary receives compensation as a percentage of deal value upon closing.

→ Triggers ITAR, Part 130, and potential FCPA exposure.

Scenario C — The Licensing Assumption Error

A party assumes that another participant’s export license covers all actors in the transaction.

→ Incorrect; brokering obligations are independent and must be separately assessed.

XIII. Conclusion

Brokering under ITAR should be treated as a core compliance risk, not a side issue. It remains a consistent enforcement priority, and regulators are increasingly focused on how deals are structured and facilitated, not just who manufactures or exports.

Labeling activities as “advisory services” or “introductions” does not create a safe harbor. In many cases, those roles alone can trigger regulatory exposure.

In practice, prior authorization, typically through Form DS-4294 submitted to the Directorate of Defense Trade Controls (DDTC), is required before engaging in brokering activity, not after the fact. This obligation can extend beyond U.S. persons. Non-U.S. actors may still fall within ITAR jurisdiction depending on how the transaction is structured and whether there is a sufficient U.S. nexus.

Compensation structures also matter. Success fees, commissions, and other contingent payments are closely scrutinized and can create standalone liability. That’s why brokering activity requires careful upfront legal analysis, thoughtful structuring, and integration into the broader compliance framework, not a post-deal check.